Automating delta adjustments through algorithmic trading

- Mar 4, 2025

- 4 min read

The financial industry has experienced a growing interest in options trading as a popular instrument. Investors operating in the Indian market now utilize options trading to establish diverse portfolios which effectively reduces their risk exposure. Options trading relies on "delta" for understanding how changes in the asset value affect option prices. Indian traders use delta-adjusted algorithmic trading systems to automate their portfolio management while achieving better performance metrics as well as enhancing their ability to handle market volatility.

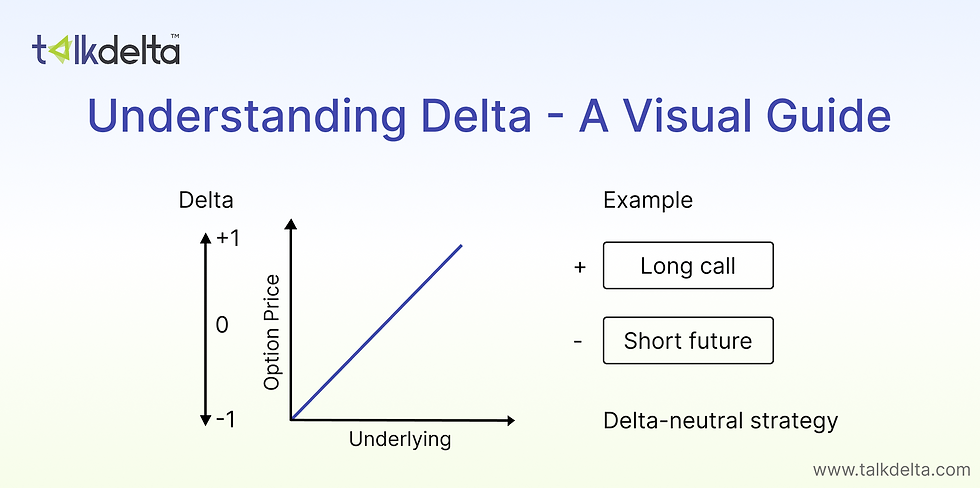

Understanding Delta in Options Trading

The financial instrument value is modified by Delta (∆) when its underlying stock or index moves by one unit. The price of a call option will move by ₹0.60 when the Nifty 50 index rises by 1 point if its delta measure stands at 0.6. The option value decreases by ₹0.40 when the index value drops by ₹1 when the delta stands at -0.4.

The delta range of put option prices falls from 0 to -1 whereas the all option delta exists between 0 and +1. The awareness of delta allows traders to predict market price movements which enables them to create proper risk management strategies for volatile trading periods.

Delta in Indian Rupee Terms

A practical implementation from the Indian stock market provides an example. With 100 units of Bank Nifty call options at 0.5 delta, your value would likely increase by Rs. 5,000 when the Bank Nifty index rises by Rs. 100. The approximate price change of your option would be:

Delta Impact = Delta × Change in Underlying Price × Number of Contracts

= 0.5 × ₹100 × 100

= ₹5,000

When you measure delta at 0.5 your options will increase by ₹5000 in market value. Through the delta metric you can accurately measure portfolio risk using basic arithmetic methods.

Why Delta Adjustments Are Crucial

The changeable nature of Delta matches trading market swings while its market value depends fully on underlying asset price changes. Outcomes result from combining time decay effects with volatility dynamics. When you trade Reliance Industries options any sudden price increase can substantially modify your delta value. The reconstruction of portfolio balance needs traders to execute delta adjustment modifications through their delta hedging process.

Challenges of Manual Delta Adjustments in India

Manually adjusting delta in a fast-paced market like India can be difficult because:

High Volatility: Trading professionals experience delays due to speed fluctuations seen in prices on Indian stock indices Nifty and Sensex.

Time constraints: Delta-neutral investors have to initiate ongoing alertness and periodic adjustments to sustain their position because they achieve neutrality.

Execution Delays: Manual controls tend to slow needed market adjustments that raise overall risk profiles.

Automating Delta Adjustments with Algorithmic Trading

The execution of real-time delta adjustment management occurs through efficient algorithmic trading operations. Automated trading strategies allow traders to:

Monitor Delta Continuously: The algorithms track shifts occurring in delta values as they monitor multiple positions in real time.

Execute Trades Quickly: Hedge adjustments executed by automatic systems finish their process within seconds thus producing very short delays.

Eliminate Human Mistakes: Algorithmic trading systems both reduce mistakes made by humans as well as systematic operations.

Implementing Automated Delta Adjustments in Indian Markets

TalkDelta provides Indian traders to automate their options trading through its sophisticated tools. Through these platforms, traders establish predetermined delta rules that help maintain portfolios within their defined risk profiles.

Key Features for Indian Traders

Delta-Adjusted Notional Value

Real trading exposure becomes clear to traders through this value. An Infosys option holder with ¥10 lakhs notional value faces a delta component of 0.7.

The delta-adjusted notional value would be as follows:

The calculation for Delta-Adjusted Notional Value requires multiplication of Notional Value and its corresponding Delta.

= ₹10,00,000 × 0.7

= ₹7,00,000

An accurate market exposure value you are at risk with amounts to ₹7,00,000 rather than the contract's notional value of ₹10,00,000.

Best Algo Strategy:

Strategies in algorithmic trading depend on the specific goal that traders pursue. Employees need different trading approaches based on their risk management needs such as delta-neutral techniques for market risk control alongside dynamic hedging techniques for active markets.

Automating Hedge Adjustments:

Full risk management becomes achievable because algorithms will automatically consider additional Greeks including gamma and vega.

Advantages of Automated Options Trading

Increased Efficiency: Automated systems are capable of processing huge amounts of market data and trading at lightning speeds.

Enhanced Accuracy: By eliminating manual errors, traders can consistently maintain portfolio performance.

Scalability: Automated trading allows an investor to simultaneously manage multiple positions in stocks, such as TCS, HDFC Bank, and SBI.

Real-Time Risk Management: The automated systems keep the portfolios delta-neutral even in volatile trading sessions.

Computer-based trading systems are changing India's options market by automatically performing delta modifications. Through advanced trading software like TalkDelta users can optimize operations while achieving portfolio equilibrium and react quickly to market fluctuations. The growing Indian stock market requires option trading automation to become a fundamental approach for traders who want better efficiency and risk control.

TalkDelta delivers optimal automated trading solutions and advanced tools specifically built to fulfil Indian traders' specific demands. Real-time delta monitoring automated hedge adjustments and custom algorithm capabilities propel TalkDelta as a leader in options trading development.

This is a really helpful explanation of delta adjustments and automated hedging strategies, especially for traders trying to manage risk in volatile Indian markets. The examples make the calculations much easier to understand, and the focus on automation shows how important speed and accuracy are in modern trading. I was actually searching for a terabox downloader online free tool earlier and somehow ended up learning more about algorithmic options trading instead!

The Ultimate Guide to Amazonian Cubensis

Looking into exotic mushroom strains? you’ve likely heard about the legendary Amazonian Cubensis. Amazonian cubensis mushrooms are well known in the shroom growing community for their dense caps and thick stems. Users have noted effects that are deeply introspective and often more vivid than common cubensis strains. ⤵️

https://hempdelics.com/product/amazonian-cubensis/

Hempdelics is one of the best dispensaries in the United States that sells legal Psychedelic Products ! Whether you’re looking for a great trip or you’re ready to dive deeper into unlocking your mind, Hempdelics got you covered. We are Best in psychedelic mushrooms and microdosing mushrooms! Order Now at Hempdelics.com

<a href="https://hempdelics.com/product/oneup-bars/" rel="dofollow">OneUp Bars</a>

<a href="https://hempdelics.com/product/5-meo-dmt/" rel="dofollow">5-MeO-DMT</a>

<a href="https://hempdelics.com/product/buy-ayahuasca/" rel="dofollow">Buy Ayahuasca</a>

<a href="https://hempdelics.com/product/psilocybin-capsules/" rel="dofollow">Psilocybin Capsules</a>

<a href="https://hempdelics.com/product/lsd-gel-tabs/" rel="dofollow">LSD Gel Tabs</a>

<a href="https://hempdelics.com/product/liquid-lsd/" rel="dofollow">Liquid LSD</a>

<a href="https://hempdelics.com/product/lsd-blotters/" rel="dofollow">LSD Blotters</a>

<a href="https://hempdelics.com/product/mdma-pills/" rel="dofollow">MDMA Pills</a>

<a href="https://hempdelics.com/product/lsd-gummies/" rel="dofollow">LSD Gummies</a>

<a href="https://hempdelics.com/product/buy-golden-teacher-cubensis/" rel="dofollow">Buy Golden Teacher Cubensis</a>

<a href="https://hempdelics.com/product/magic-mushroom-grow-kits/" rel="dofollow">Magic Mushroom Grow Kits</a>

<a href="https://hempdelics.com/product/arenal-volcano-cubensis/" rel="dofollow">Arenal Volcano Cubensis</a>

<a href="https://hempdelics.com/product/blue-meanies-cubensis/" rel="dofollow">Blue Meanies Cubensis</a>

<a href="https://hempdelics.com/product/penis-envy-magic-mushroom/" rel="dofollow">Penis Envy Magic Mushroom</a>

<a href="https://hempdelics.com/product/amazonian-cubensis/" rel="dofollow">Amazonian Cubensis</a>

<a…

Prepare your company with Security Health Check available from Ascent InfoSec. We’ll pinpoint your security vulnerabilities and help strengthen your protection. Ascent InfoSec Security Health Check can help you assess your current level of incident preparedness, review your response plan, recognize existing breaches and identify possible security vulnerabilities in your infrastructure. Knowing the challenges your organization faces removes the guesswork, and is the first step toward protecting vital company assets and customer information. The digital transformation of business introduces both opportunities and risks. Mitigate breaches and potential risks with proven tactics performed by a team of security experts.

Security Health Check combine on-site methods, Internet traffic-pattern analysis, and the expertise of our Ascent InfoSec Threat Advisory Team to help you better…

If you're serious about automated trading and want expert guidance, check out Push Button Trading. They're certified professionals in push-button trading solutions, available 24/7, and offer upfront pricing so you know exactly what you’re getting. Whether you're just starting or scaling up, they can help you avoid common pitfalls and maximize the performance of your bots.